Tesla, made in China

50% of Tesla productions are now in China

Hi, disruptors,

This is a bonus issue on Tesla’s new reality that is irreversibly intertwined with its Chinese production capacity. This trend is apparent in many industries and the root cause is pretty obvious - the growing Chinese consumer market & the efficient Asian supply chain. Currently, the Chinese consumer market is roughly equal in size compared with that of the USA, and in about 10 years, the Chinese consumer market will be twice it is now. This reality underpins our world’s economic order, which means despite the rhetoric of decoupling and confrontation in the political sphere, there is a strong magnetic force, at least within the business community, to pull China and the U.S. together.

Let’s explore a part of that reality today with the auto industry.

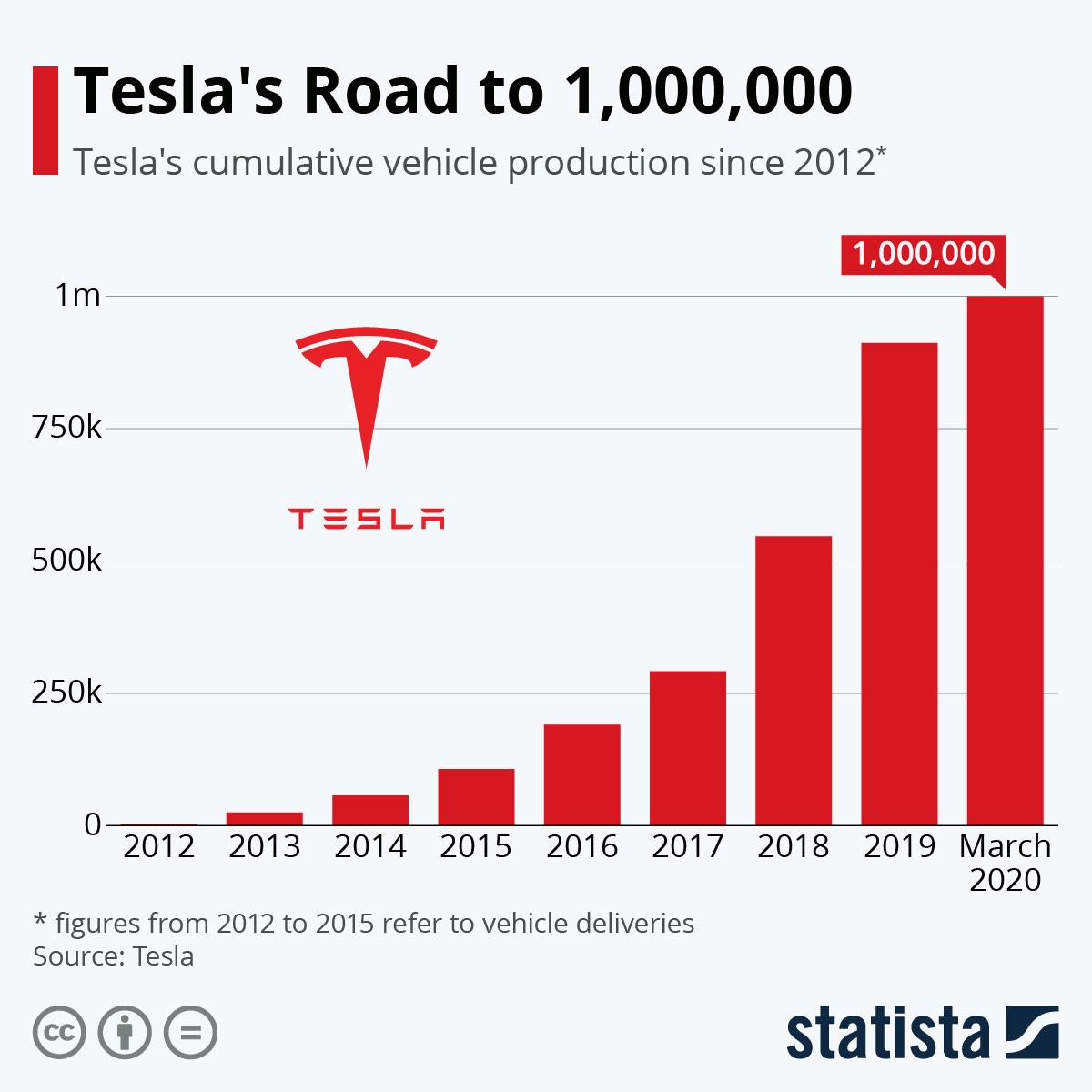

In 2021, Tesla delivered 936,000 cars, the majority of which are Model 3s and Ys.

I can remember a time when it was hard for Tesla to produce and sell just 100k cars, and now it is closing in on the magical 1 million number. All of this happened in a short span of a year.

It took Tesla over 10 years to produce its first 1 million cars, and 1 year to produce the second 1 million cars, the rate of improvement is astonishing.

But here is the elephant in the room: China.

While closing in on 1 million cars delivery is a huge achievement, what is more striking, in my opinion, is how quickly Tesla’s China market and China-based production has improved. In fact, in 2021, half of the Teslas sold were made in China. So Tesla’s tremendous improvement in production column in 2021 is not as much an achievement of Tesla as a testament to the so-called “Chinese speed”.

According to Reuters’ calculations of CPCA’s data, Tesla’s total sales of China-made cars for last year [2021] was at least 473,078, which means virtually all of Tesla’s production improvement came from Giga Shanghai. Moreover, Tesla has reported that its Giga Shanghai production capacity has now exceeded 70,000 cars per month, this means it’s very possible that Tesla will be able to reach its 1 million Giga Shanghai production goal in 2022.

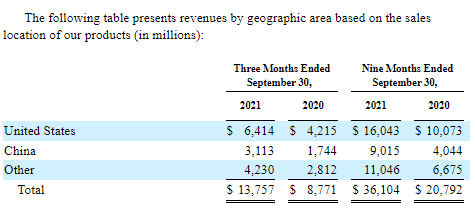

Correspondingly, Tesla’s sales in China also rose to almost half of Tesla’s U.S. sales to 3.11 billion dollars, Tesla’s sales effectively follow the 3 economic poles of the world, the U.S., Europe, and China.

I need hardly remind everyone who’s following Disrupted that Tesla’s Shanghai factory only started construction in January 2019. Here is a brief timeline of Giga Shanghai,

29 Dec 2018, Shanghai government grants Tesla permit to build Giga Shanghai

Jan 2019, the groundbreaking ceremony of Giga Shanghai

Aug 2019, Giga Shanghai completes construction

Oct 2019, Giga Shanghai production begins

In 2020, Total Tesla delivery worldwide: 509,000

In 2021, Total Tesla delivery worldwide: 936,000

Not only was Tesla ahead of schedule to construct Giga Shanghai, but it was also built for approximately 65% less capital expenditure per unit of manufacturing capacity than had been the Model 3 production system in the US. Basically, all of Tesla’s incremental production, which is now half of Tesla’s production come from Shanghai, and a significant of these Shanghai-produced Teslas are sold locally.

Remember of production hell Elon Musk whined about in 2018 when it comes to Tesla’s Fremont factory? Not only is this “production hell” non-existent for Giga Shanghai, but it is also on track to produce 1 million cars in its 3rd year of production (possibly). No wonder Elon Musk, who is famous for his government trash talks, kept his mouth shut when it comes to the CPC.

But surely, with China now accounted for over half of Tesla’s production and possibly in a few years, sales, what are the implications?

EVs on a fast track

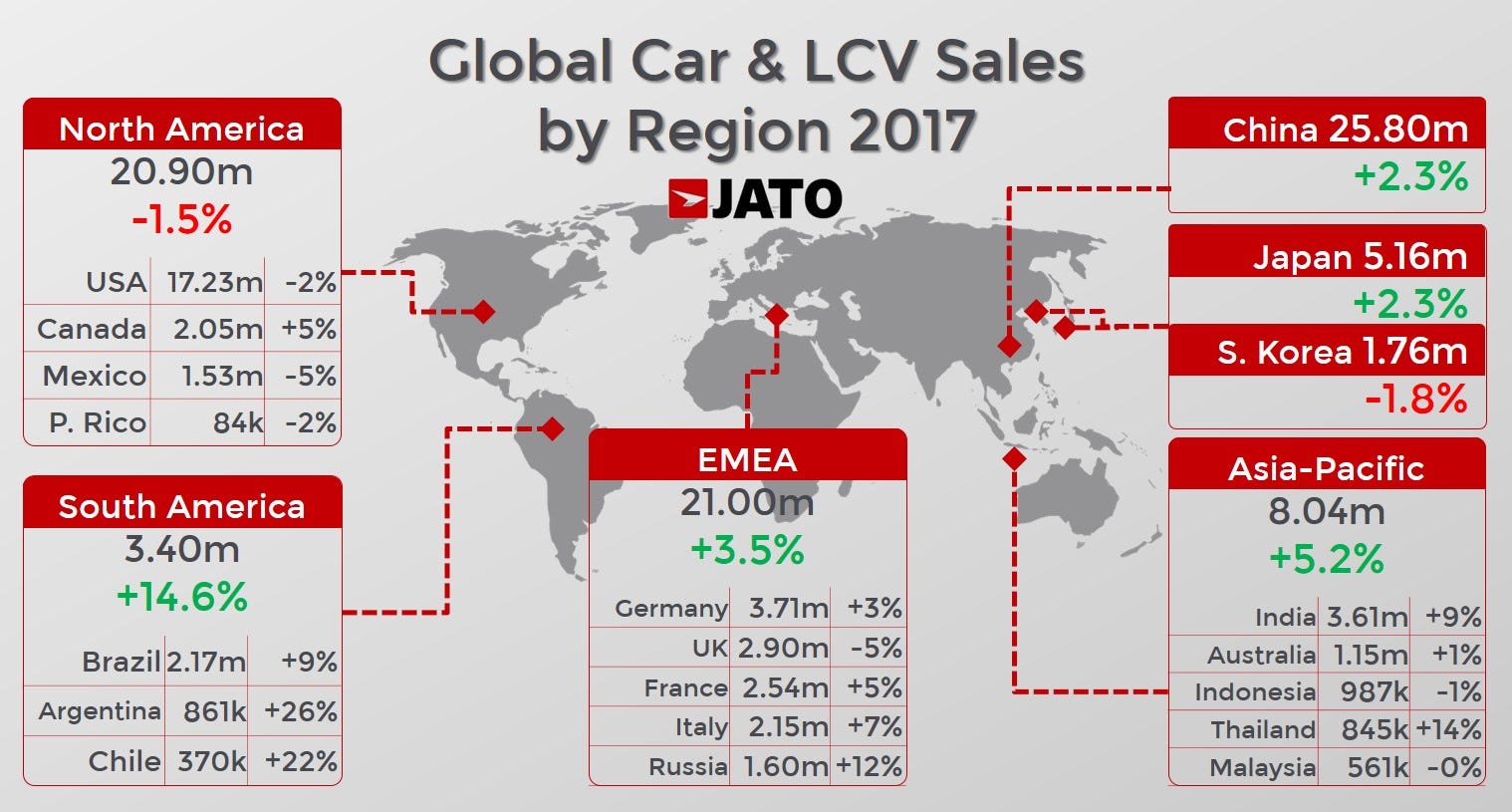

The first implication in my opinion is an EV industry on steroids. Industry analysts put EV industry CAGR at around +25%, which means the industry will double every 3 years. This is an impressive number, but I believe this is prediction is too conservative for Tesla. After seeing the resounding success from Tesla’s shanghai factory, it would be unreasonable for Tesla to stop at one Chinese factory, and indeed rumors are already spreading indicating another Tesla factory in China. Some of you may want to remind me of Giga Berlin, and I’ve not forgotten that😉, Giga Berlin is an industry-standard practice to set up a production center near the demand, and looking at the auto demand around the world, it’s obvious that the 3 demand centers of automobiles are in North America (20 mils), Asia (40 mils) & Europe (20 mils).

This graph shows clearly where the future is for auto demand. Asia’s total auto demand is the combined demand of both North America and EMEA, this means Giga Berlin is going to be an important production center for Tesla in Europe, but will probably not do much outside of that region.

If we look at Giga Shanghai’s production and sales, half of Giga Shanghai’s production is sold outside of China in the US and EU, which may remain the status quo for a while. Depending on how quickly Giga Berlin/Austin can come online, Tesla’s Chinese factory will supply the world’s demand in the meantime. Considering that over 90% of components in Tesla’s Chinese production are sourced within China, this will be a powerful boost to the quality of EV suppliers in China.

But why would the combination of Tesla & China put the EV industry on a fast track?

There are two reasons for this.

Firstly, supply and demand. Needless to say, the market for EVs is huge, basically the entire consumer auto market. Cars are consumer discretionary goods, and their demand is swayed heavily by consumer sentiments and trends. In 2022, buying a Tesla EV is not just fashionable, it is the politically correct thing to do. It’s a fact that EVs, throughout their lifetimes, are lower carbon emitters than their internal combustion engine counterparts. Tesla is the leading company that has excelled in managing this consumer demand, and what Tesla lacked is a powerful supply chain that can channel this latent energy of EV demand to actual sales. Therefore, the collaboration with China solves Tesla’s biggest problem, its production difficulties.

On the other hand, the same latent energy has also been accumulating on the Chinese side, local EV companies, suppliers of batteries, and other EV components have also been trying really hard to sell to the premium US and EU market, on top of that, the Chinese government has subsidized EV related industries for years. With Tesla, these suppliers can finally channel their latent supply capacity to actual sales and revenue.

It’s a win-win for both.

Secondly, there are 3 powerful effects at play.

Technology stack disruption is the first one. Needless to say, EVs and internal combustion engine (ICE) cars are from two different generations of technologies, they are built upon 2 different technology stacks. When a disruptive technology was conceived, its product offering is often inferior due to the lack of economies of scale. However, once the critical technology performance threshold is crossed, the older technology withers very quickly. Digital vs. film cameras, the smartphone revolution, and the post mail industry to name a few.

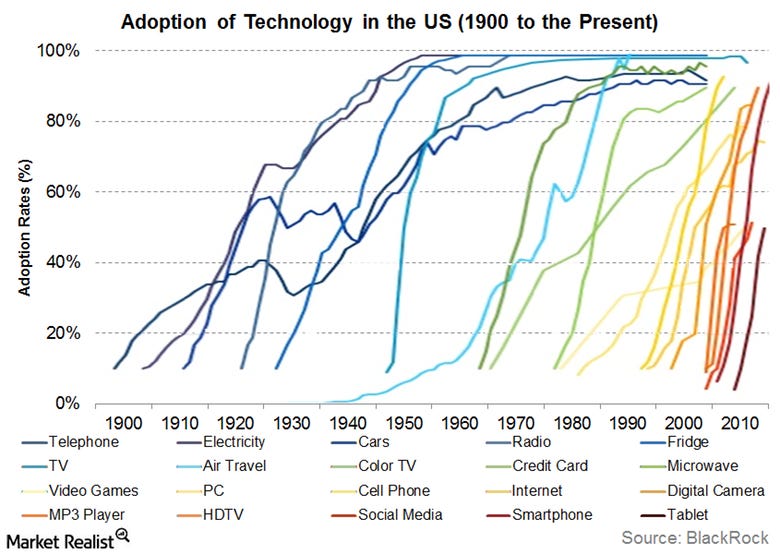

Furthermore, new technology adoption speed has accelerated thanks to the Internet and social media. As you can see below, the slope of tech adoption says it all.

Due to the automobile industry’s complex supply chain and technology, EV adoption has already been delayed for many years, 2021 was the turning point.

Additionally, this process is irreversible as the root cause of disruption is fundamental and irreconcilable. Disruption is a dilemma where incumbents often fail to deliver despite their full awareness that they are getting disrupted. I categorize this disruption dilemma into 5 phases. The Emergence, The Grind, Performance parity, The Gridlock, and Nirvana.

The Emergence. A start-up enters a mature industry with a ‘silly’ idea that is completely against the industry fundamentals. These entrepreneurs often lack an executable roadmap, what they have is simply a vision, or what the critics would call, a “pipe dream”. Nevertheless, the founders’ ideas are logically coherent, scientifically sound, and are based on first principles.

The Grind. In this phase, the emerging startup faces tremendous challenges and adversity, the first of which is its inferior product/technology offering and the high cost of production. A case in point is Tesla, it used its first-gen 200k roadster to break into the niche market as a POC essentially. In this phase, some venture capital funds will notice the new startup, see the potential of the industry and inject funds. These capitals love risks and are critical to creating a relatively leveled playing field for competition.

Performance Parity. The emerging technology catches up with the incumbent. The tide turns, industry insiders start to vote with their feet, while the consumers are slow to react as the product offering and technology level is the same.

The Gridlock. This step is characterized by the incumbents’ awareness of the paradigm shift but are nevertheless unable to adapt. Why gridlock and unable to change? Take traditional ICE auto companies as an example.

Competence mismatch. ICE talent & ICE supply chain is now rendered worthless, years of training and technology development become a sunk cost. Here is a GM leadership’s resume page, much of their experiences are no longer relevant in the EV world, not to mention the transmission engineers who are now managers at GM, whose skills are worthless in the EV world.

Leadership incentives are misaligned. Most public company executives’ salary is tied to their stock prices which are then tied to sales and revenue. Making drastic shifts to EV means definite loss of revenue & increase cost in R&D. No professional company executives will forgo their bonuses to fight for the company’s fate in 10 years.

Adverse capital market. Every big fund manager is now eyeing eating traditional car companies alive, auto is a trillion-dollar industry.

Nirvana. A new industry is established with an entire ecosystem of suppliers, technology stacks, new opportunities, and new synergies with other industries.

The auto industry is now gridlocked in phase 4, traditional car companies are declining quickly as most of them have given up on making batteries. This means giving up on the core technology in an EV and hence giving up their negotiation power in future profit wars. Battery patent holders in Japan, Korea, and China will dominate battery negotiations. This is just one example, internal structural imperatives make it really hard for incumbents to shift to EV decisively, but going slow is sometimes just as harmful. In a fast-moving industry, inaction (going slow) will usually lead to a prolonged death instead of a smooth transition.

One thing that is on the traditional auto OEM side though is brand loyalty and their control over sales channels, whether these will give them enough time to change, and if they will be able to overcome the gridlock, it’s yet to be seen.

The other two effects are the network effect and the Matthew effect. The network effect will make sure consumers, suppliers, and employees slowly in the traditional car industry slowly but surely shift towards the EV industry in pursuit of a better product, profit, and a better future respectively. The deteriorating profit of ICE car companies will mean less money to hire quality people to compete with the engineering quality of EV companies as well.

Matthew effect will also accelerate both Tesla and an entire ecosystem of suppliers in the US & China. The best EV company will get better faster and of course, along with the supplier in its ecosystem. In the case of Tesla, these suppliers are in China & the U.S. Germans should be worried as auto takes 10% of Germany’s GDP, so should the Japanese.

4 critical factors of production include labor, capital, land, and information are now on Tesla’s side. I don’t need to explain to this audience how much capital is flowing to the EV industry, all one needs to do is to check the stock price of Tesla and other EV-related companies to get a feel for that.

A world increasingly reliant on Chinese manufacturing

The combination of what China can do in manufacturing and what Tesla can do in tech disruption is absolutely powerful. But how will this affect the US, China, and the world?

First of all, China’s manufacturing dominance will continue. As countries develop, it usually goes through a financialization process shifting manufacturing overseas. A case in point is the US, once accounted for half of the world production (after WWII), US manufacturing % of GDP is now at a meager 11%, she has decided to financialize domestic companies and industries. However, China is not choosing a different path. In China’s 14th five-year plan, it has recognized its dropping manufacturing as an issue for China’s employment. Manufacturing as a % of China’s GDP is now at 27% which is similar to that of South Korea, but China is still a much poorer country than South Korea on a per capita basis. So, the direction from the CPC of China is to maintain the manufacturing % of GDP for now and to upgrade the technology at the same time.

This process is also exacerbated by COVID, I will not elaborate on this, but here are a few articles you can read to get started.

China's trade surplus hit an all-time high amid the pandemic, rising 30%.🤣🤣

Tesla’s China development is a high-profile case of how interconnected U.S. industries are with China. The relationship is intricate, delicate, and synergetic, but as China grows to its current behemoth size of 18 trillion in GDP, and its technologies are more advanced, competitions are on. How could this be managed? It is for the wise leaders of the two countries to decide.

For Tesla, its priorities are simple: profit, profit, and profit!