Xiaomi, how an empire is built

Xiaomi, how an empire is built

After Huawei's fall, can Xiaomi make it?

Welcome to the 40+ of you who joined us last week. If you have not signed up yet, join +381 smart, curious, and critical people by subscribing here:

Hi friends👋,

Another week has passed and the COVID situation is getting worse… again, hope all of you are doing well. Drink lots of water and stay healthy! I just had my second dose of Pfizer vaccine, having a bit of a headache right now as I type this. People tell me that’s cuz I’m young and my immune system is functioning well, which is comforting I guess.

Last week I had an interesting conversation on Twitter regarding the possibility of turning off THE YouTube Algorithm. It honestly feels like a capital “A” for me as The Algorithm is now everywhere, all the time, capitalizing on our emotions, deciding how we should spend our private moments. Would you press the button to turn off the algorithm? I would. It is an open secret that YouTube’s algorithm prioritizes Watch Time, but what does that lead us as a society? It leads YouTube to superb revenue growth I have no doubt, but recently, videos that get recommended to me are getting polarizing, and I just realized this has been the case for a while now. I can only imagine our children hooked on this.

Maybe we can learn a thing or two from the Chinese Cyberspace administration this time.

Anyways, let’s get into our topic of today, Xiaomi.

Xiaomi, how an empire is built

2021 is the 11th year since Xiaomi’s founding, as of today, Xiaomi is one of the fortune 500 companies with an 82.5 billion dollar market capitalization. Its product lines span the whole landscape of consumer electronics. You may know it as a smartphone company, but it also makes smart pressure cookers, smart washing machines, smart desk lamps, and now, Xiaomi is building an electric car. At its peak in December last year, Xiaomi crossed the 100 billion market cap. It took Xiaomi exactly 10 years to do that.

Infosys took 40 years to reach a 100 billion market cap

Apple took 31 years to reach a 100 billion market cap

NVidia took 24 years to reach a 100 billion market cap

Microsoft took 21 years to reach a 100 billion market cap

Xiaomi took 10 years to reach a 100 billion market cap

Xiaomi is now bigger than Twitter, Snapchat, Uber, eBay along with many other companies birthed in the mobile age.

It is my aim to unravel the complexity of Xiaomi’s ecosystem strategy and explore its vision for the future, to show you the Xiaomi behind its smartphone operations, as well as to look into the future for Xiaomi’s EV push.

I will cover Xiaomi’s past, now, and the future. Let’s dive in.

A Pig that was meant to fly

Lei Jun, the founder of Xiaomi, was not unfamiliar with running a business when he started in 2010. We’ve heard of many inspiring entrepreneurial stories, and most of them start with a founder who has no experience, but with extraordinary hard work and ingenuity, disruptions prevail. Mark Zuckerberg started Facebook in his dorm room, Steve Jobs started Apple in his parent's garage, and Jack Ma was a school teacher before he founded Alibaba.

Ignoring the fact that Mark went to Harvard, Steve grew up in Mountain View California in the 60s America, and Jack Ma was a College teacher in one of China’s most wealthy cities in the 1990s, I guess we could say they are “self-made stories”.

Lei Jun was different. By the time he started Xiaomi in 2010, he’s already a multi-millionaire, with experiences taking Kingsoft to IPO, selling Joyo.com to Amazon for 75 million dollars, and he was already a successful venture capitalist invested in JOYY Inc, and UC browser, and more. He can do it differently.

The team he built was world-class.

Xiaomi’s dream team (from left to right)

Huang Jiangji. Microsoft, he oversaw the development of products such as the Chinese version of Windows Mobile, Windows Phone 7 multimedia, Internet Explorer, and instant messager.

Liu De. He graduated from Art Center College of Design and received a master's degree. Liu De returned to China and founded the Industrial Design Department of Beijing University of Technology.

Zhou Guangpin. Motorola, expert engineer. Doctor Zhou was the Chief of hardware R&D of Motorola's best-selling model "Ming" series.

Lin Bin. Microsoft & Google, Director of MSRA. He participated in the R&D of products including Windows Vista and IE8. He was also the engineering Director of Google Global. He was responsible for building and managing Google China’s Mobile Search and the Android App Localization teams.

Lei Jun, Founder & CEO of Xiaomi.

Li Wanqiang. Kingsoft, Lei Jun’s right-hand man. Li Wanqiang served at Kingsoft in various positions as Cheif Designer of UI department, Director of Design Center, and Director of Internet Content.

Hong Feng. Google’s Engineering lead oversaw the development of Google Calendar, Google Map, and Google 3D Street View.

All founders came with an exemplar track record with great resources at disposal. Lei Jun represented a different generation of Chinese entrepreneurs. The pre-2010 startups in China mostly focused on software, Tencent was founded on a messaging platform and Alibaba was an online e-commerce store, even Lei Jun’s Kingsoft and Joyo.com were essentially software and website companies. The truth is, Lei had no idea how a smartphone is made, he had to assemble this team in order to make Xiaomi work.

But, why did he enter the smartphone market if he is so inexperienced?

Here we need to talk about Lei’s famous flying pig theory. He started in the Internet sector of China in 1993 and led an incredibly successful career taking Kingsoft to IPO in 2007. In ordinary people’s eyes, Lei is successful, but what Lei asks himself often was “why was I not able to create a company like Alibaba or Tencent?” After all, when Lei Jun started, neither Jack Ma of Alibaba or Pony Ma of Tencent was anywhere to be found.

According to Lei Jun’s flying pig theory, that is because Kingsoft was not in the “Fengkou”, which is literally translated to “wind gap”, but in this context, it means trending industry verticals. He theorizes market trends as the “wind” and the “gap” are the strategic positions, companies should aim to position themselves on these “wind gaps” because “even a pig can fly if it stands at the center of a whirlwind,” he says.

Ridesharing was an example where billions of dollars were poured into an industry in the span of 5 years, created many billionaires. None of them are profitable today. EV is another vertical that is on the uptrend right now, NFT is another.

Lei Jun believes that the reason why Kingsoft was not another Alibaba or Tencent in China because it was in the wrong vertical. For his next company, he needs to find the vertical that can support a 100 billion-dollar company, and that vertical was Mobile Internet (MI).

Not only was Lei right, Xiaomi’s rise changed the entire smartphone industry of China. Founded in 2010, Lei Jun launched Xiaomi at the right moment. Why? Essentially, there were two reasons.

Timing. The smartphone industry was getting disrupted. Previous capabilities have become obsolete. LG, Nokia, Sony Ericsson, Motorola, these are dead brands coming out of this disruption. Smartphones depend heavily on powerful IC, large screens, and RAM, market incumbents do not have the capability.

China. According to NBS, Chinese per-capita annual disposable income in 2010 was 10,046 RMB, however, when the original iPhone came out in 2007, it cost 500 dollars with a two-year telco contract, which meant 5,000 RMB per iPhone for Chinese consumers after taxes and fees. This is not affordable for most Chinese at that time, which created a high demand for low-end Apple-like smartphones. Remember the narrative of China creating knock-off smartphones? That narrative has now faded, but if anyone is counting, Xiaomi started it. Moreover, Shenzhen China was also on its way to claim the title of the “hardware capital of the world”. All of this enabled the first Xiaomi to tap into a ready audience for a 2000 RMB Apple-like smartphone.

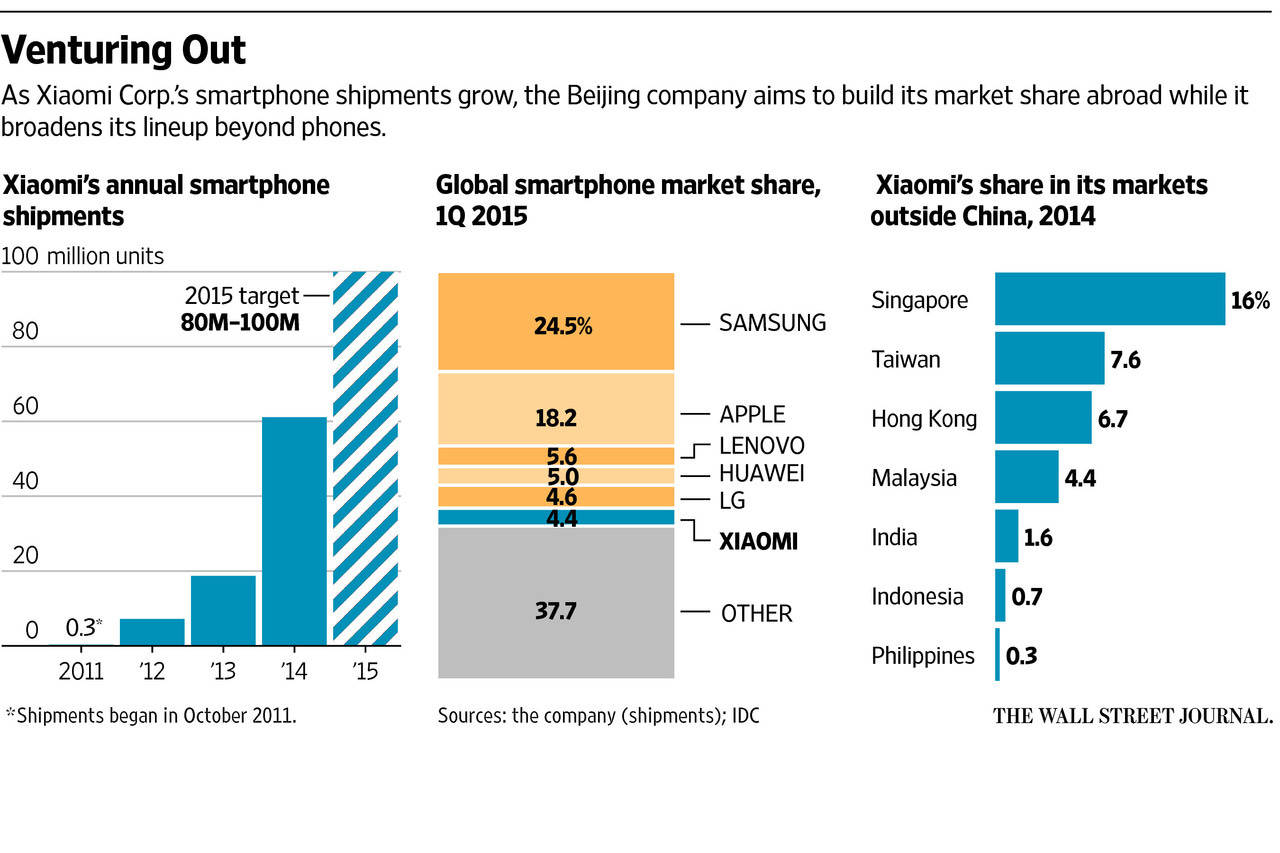

Xiaomi sold 300k units in 2011, over 1 million in 2012, close to 20 million units in 2013, and in 2014, Xiaomi sold over 60 million units of smartphones.

By Q1 2015, Xiaomi along with the Chinese smartphone makers are emerging, taking in 15% of the global smartphone market.

Since 2015, Xiaomi’s annual revenue rose from 60 billion RMB to over 240 billion RMB in 2020.

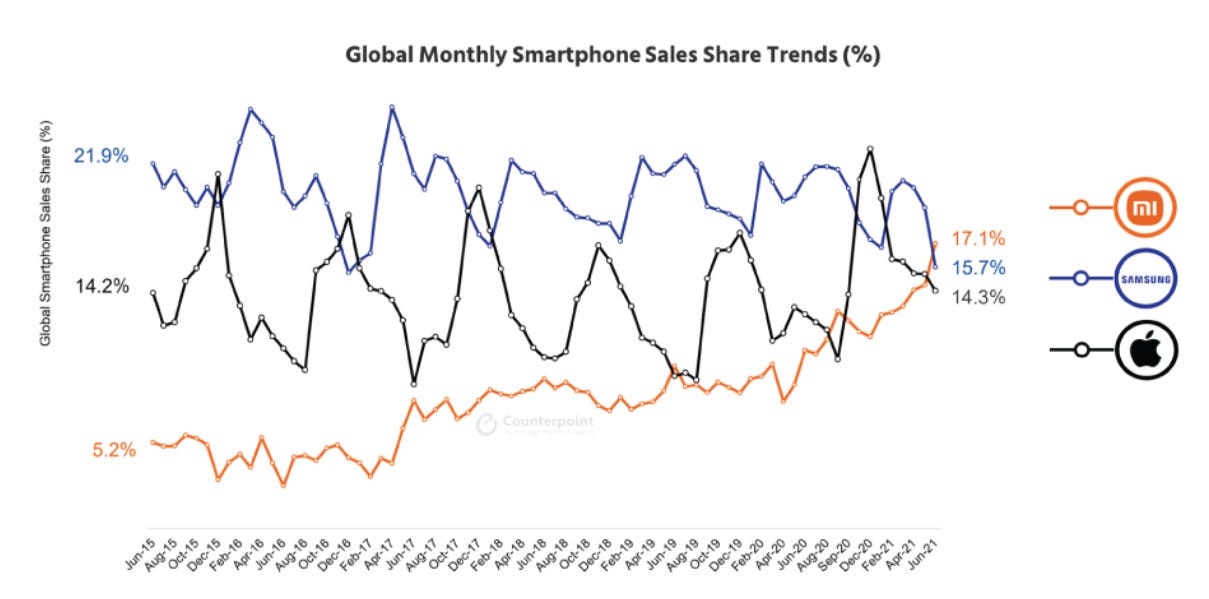

In June 2021, Xiaomi’s global monthly market share rose to overtake Apple and Samsung to achieve number 1 status, this is the first time a Chinese company has pulled off this feat. Xiaomi claims 17.1% market share whereas Samsung and Apple take 15.7% and 14.3% respectively.

What can we learn from Xiaomi’s rise?

Lei Jun’s “Fengkou” theory captured the zeitgeist of the capital market today, and he found the right timing for a smartphone business in China. If Lei had started in 2007, the Chinese smartphone supply chain was not mature enough, neither was the Chinese market big enough. If Lei had started in 2015, the opportunity window would be closed.

Xiaomi is competitive in the android market, it is able to challenge Samsung in the vacuum that’s left by Huawei. If there is no more ban from the U.S., Xiaomi could potentially cement this lead over Samsung and apple.

Apple still has a solid market share among the high-end mobile user segment. Xiaomi’s high-end smartphone(defined as > 4000 RMB, which is over 600 dollars) shipment was at 5.77 million units in 2020, comparing to Apple’s 200 million units shipment per year.

That leads us to where we are today.

Xiaomi Today

Xiaomi’s business lines are as follows

Over 60% of Xiaomi’s revenue comes from its smartphone sales in 2020, a steady increase from 2019. This increase is attributed to Xiaomi’s rise in popularity in Europe, its overseas revenue growth was at +34.1% in 2020. In total, 146 million units were shipped globally, 10 million units are premium smartphones (defined as more than 3000 RMB, which is around 500 dollars).

IoT and lifestyle products include smartphone pressure cookers, umbrellas, and more accounts for 27.4% of total revenue in 2020, an increase from last year, but a decrease in group revenue share. Xiaomi highlighted “strong growth in demand of certain IoT products, such as robot vacuum cleaners, routers, and TWS earbuds”

Internet services have improved by over 7% to 23 billion RMB, attributed to growth in the advertising and gaming business. This is where MiUI comes in the Xiaomi user interface, through MIUI (400 million MAU globally, only 114 million are from China), Xiaomi is selling ads (12.7 Billion RMB), TV subscriptions (4.3 million paid subs).

Now, about Xiaomi’s profit margin. Profit skews heavily towards services sales.

Xiaomi’s smartphone business has a 7.2% gross margin and low single-digit net margins. IoT and lifestyle has a 12.8% gross margin and lower net margin. Xiaomi Services has a 61.6% gross margin and 45-55% net margin.

So, Xiaomi’s profit model basically is to leverage low margin hardware sales to drive high-profit services sales. This has a problem as Leon pointed out in this post, that the service attaches rate may be low for Xiaomi’s overseas business. (Google is blocked in China)

The Internet services business takes advantage of the Android store being blocked in China, giving consumers a place to download ads and a payment platform.

Overseas revenue rose +34.1% in 2020, which is now 49.8% of Xiaomi’s total revenue, making it a more resilient business than most Chinese companies that focuses only on China. However, this increases Xiaomi’s revenue exposure to a possible U.S. ban (again).

Below is Apple’s revenue segmentation in comparison.

In comparison, Xiaomi is not competitive in the computers, & tablets market (two top business lines for Apple). This reflects Xiaomi’s Achilles heel in essence. In the premium gadgets market (smartphones, PCs, and tablets), Xiaomi has a low gross margin (~7%), and though Xiaomi’s IoT and lifestyle devices do have a higher gross margin (~13%), it is not as significant in absolute dollar terms compared to premium gadgets. Xiaomi’s pressure cooker is sold for 40 USD, and 13% of 40 dollars is just 5 dollars, Apple’s products like Mac, iPad, and even AirPods all have their profits in the hundreds of dollars.

I wrote extensively about why Apple is able to capture huge profits in this letter.

What does Xiaomi see in its future?

Essentially, Xiaomi follows a T-shaped strategy, deepening its capability in the smartphone vertical, and broadening its product offerings to build the Xiaomi ecosystem.

Xiaomi does this through investment and R&D primarily. The company could improve its product and broaden its offering through R&D, but here is an R&D spending comparison of leading smartphone companies.

Alphabet. Alphabet spent $27.57 billion on R&D, which is equivalent to 15.1% of its revenue of $182.57 billion during fiscal 2020.

Huawei. During fiscal 2020, it spent around ¥141.893 billion on R&D, which is equivalent to $22.04 billion. Its R&D spending constituted 15.9% of its total revenue of ¥891.37 billion in fiscal 2020.

Samsung. Samsung spent ₩21,229.2 billion (equivalent to $18.75 billion) in fiscal 2020, which constituted 9% of its sales.

Apple. During fiscal 2020 (Apple’s fiscal year runs from October 1 to September 30), Apple spent $18.75 billion on R&D, equivalent to 7% of its net sales. In the first six months of fiscal 2021 (October 2020 – March 2021), Apple reported its R&D spending at $10.42 billion.

What about Xiaomi? Xiaomi invested RMB9.3 billion in R&D in 2020, which translates to just around $1.4 billion, This is just 10% of what Huawei is spending, 15% of Samsung and Apple’s R&D budget.

(Sidenote: this is why I think the U.S. decided to lift the ban for Xiaomi in May, because Xiaomi, consciously or not, decided to not compete directly with chip makers in the US, hence it is not a “national security” concern. In the long run, Huawei’s drop in sales will also result in less spending capability on R&D, making it less competitive. The Chinese gov will do everything to fight back.)

But it is not to say that Xiaomi is happy with the lower-end mobile market. Again, I wrote extensively on why Apple gets to keep enormous profits that other smartphone makers can only dream of. In summary, companies like Xiaomi must break the chain of Qualcomm (hardware chokepoint) and Android (software chokepoint) in order to really compete with Apple on profits. Samsung has tried and failed to do this in years, I believe the current geopolitical reshuffling of the supply chain is the best opportunity for Xiaomi.

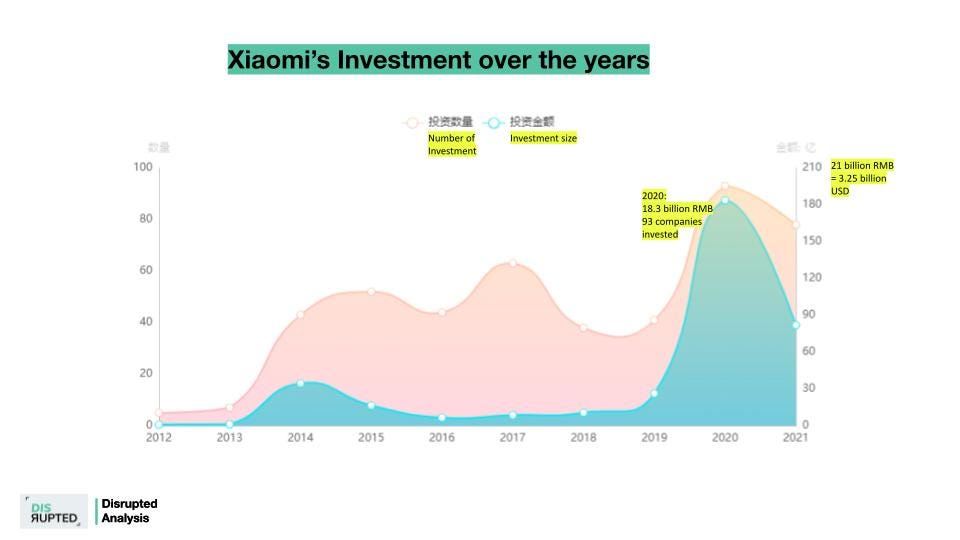

Xiaomi itself is breaking this chain through investment (Xiaomi’s Corporate VC). Xiaomi deployed 3 Billion USD into 93 companies in 2020, and if we take into consideration Shunwei Capital’s investments (Lei Jun’s personal VC fund), we may add another 500 million USD into the mix.

Xiaomi’s CVC investment is by no means an excuse for its lack of spending on R&D, but it shows us Xiaomi’s focus. (i.e. Xiaomi’s vision for its future).

Xiaomi’s investment vertical concentrates in

advanced manufacturing and smart devices,

the third-largest investment vertical is cloud,

and after that e-Commerce.

This is followed by auto, finance, gaming, sports, and etc., mostly consumer-oriented companies.

This is the T-shaped development strategy I mentioned at the start of this section, deepening Xiaomi’s capability in the smartphone vertical through investing in semiconductor companies, and broadening Xiaomi’s product offering through investing in smart devices companies. This is clearer when we dive deeper into individual investment verticals.

Semiconductor (Advanced Manufacturing)

The above is Xiaomi’s top investment ranked by size of investment in the advanced manufacturing vertical. Capital is deployed towards the smartphone vertical, from camera solutions to AMOLED driver IC to AI chips to DRAM, Xiaomi is investing heavily into the vertical. Much of the investment focus on mid to low-end semiconductor capabilities in the 45 - 180 nm nodes. Advanced chips like M1 and Kirin are at 5nm node, Xiaomi’s latest Mi 11 uses 5nm chips from Qualcomm.

I have yet to see Xiaomi’s fabless chip effort that can rival Apple’s M1 and Huawei’s Kirin. This is perhaps the biggest weakness of Xiaomi’s capability in the smartphone value chain. This may be a conscious choice seeing the consequences of the Huawei ban. Xiaomi’s total investment here is around 10 billion RMB.

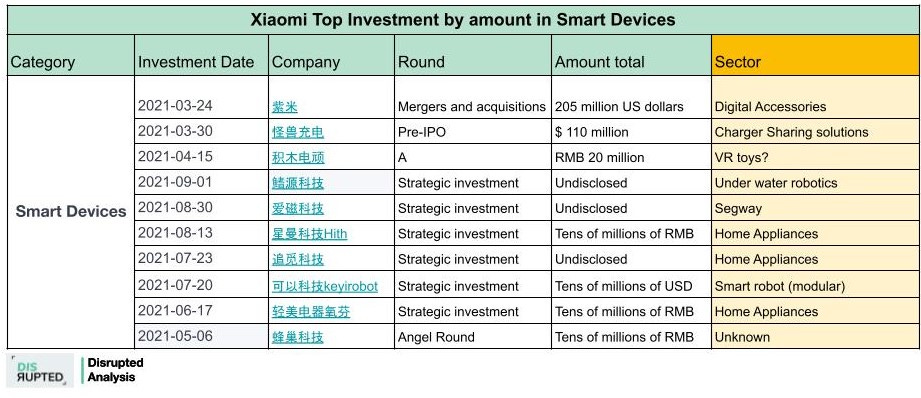

IoT (Smart Devices)

Under IoT, Xiaomi’s investments focus on its ecosystem play with the aim to bring the company into the Mi ecosystem of home appliances, accessories as well as personal products. Internet of Things (IoT) is a hype word that companies use when they want to charge a higher price for the same product, the capital market reacts better with an IoT company than with, let’s say, a pressure cooker brand. I have been hearing the word “IoT” for 5 years since I took my first job to work for a venture capital firm, I heard from my supervisor then that he started hearing about “IoT” 3 years earlier. I have yet to see a true revolutionary “IoT” application in the consumer vertical.

Most people living outside of China underestimate the diverse product offerings of Xiaomi’s ecosystem, this website gives you an idea of what this “ecosystem” offers. You can also see that in the picture below,

Xiaomi calls it MiOT, Xiaomi Internet of Things. It includes smartphones, sports cameras, drones, headphones, suitcases, VR toys, and even bed linens. These are under Xiaomi’s IoT and lifestyle business line, the total investment size is around 10 billion RMB.

Auto (10 Billion in 10 years)

This is a new vertical Lei Jun just ventured into, it is years in the making. If you want to understand why Lei Jun is doing this, you should check my analysis of Apple’s strategy.

Little is known as to how Xiaomi is going to approach its EV, here are some of my thoughts. With 10 billion USD investment in 10 years,

Xiaomi will not be able to build its own factories for manufacturing.

Xiaomi will not be able to build its own chipset for autonomous driving, it will probably buy NVidia’s or Mobieye’s system and integrate them into the design.

Most possibly, Xiaomi will approach EV production like how it approaches smartphone production, outsourcing capital heavy manufacturing, build software systems by itself. This is different from Tesla’s OEM model where Tesla builds EVs in its own factory.

Conclusion

Thesis point 1: Xiaomi’s rise and fall and rise again in market share over the years proved its capability in strategic planning & customer management. Xiaomi will cement its top three positions in the smartphone market in terms of sales volume, but Xiaomi will not be able to challenge Apple in the premium smartphone market share, which is solidly above 1 billion active users. Xiaomi will continue to devour Huawei’s premium market share with Oppo and Vivo within China, and it will take a bigger premium share in Europe as seen from the strong demand this quarter. This will push up Xiaomi’s profitability in the smartphone business.

However, Xiaomi’s ceiling is Samsung & Apple. It will not surpass them in premium market share because of its lack of commitment in R&D. Xiaomi outsources its IC to Qualcomm, its screen to Samsung, its manufacturing to Foxconn & BYD, and its OS is from android. This business model meant that Xiaomi has little control over its supply chain. Foxconn for instance will always favor Apple over Xiaomi and TSMC will reserve its top processing node (5nm - 3nm) capability to Apple since Apple pays much more than other partners.

Thesis point 2: IoT will be an important driver in revenue and profit for Xiaomi. The Chinese GDP is projected to grow at 5 - 6% per year for the coming decades, together with an RMB appreciation at around +4% a year, assuming Chinese RMB follows the post-industrialization Japanese Yen or a post-war German Mark. China’s GDP will double in 2035. People in China will have significantly higher disposable income for premium home appliances, pushing up Xiaomi’s revenue for ecosystem products.

Thesis point 3: EV demand goes through the roof. The sky is the limit for this vertical. In my analysis for hydrogen energy, I laid out our governments’ plan to go carbon neural by 2050 and China by 2060. Starting from policymakers, the shift to EV is now inevitable. Tesla has solidly cemented its lead with half a million EV sales in 2020, and the incumbents have lost their edge falling behind Chinese and Japanese companies in both battery production and EV power systems. The traditional OEMs therefore may be pushed upstream to become tier 2 or tier 3 suppliers where brands like Apple, Xiaomi, Xpeng, and NIO will take the lead in the EV market. Battery and autonomous driving systems technology has become an important battleground for this industry.

China now has the combined auto demand of the U.S., and Japan, the EV company that gets China and the U.S., gets the world.

Xiaomi’s experience in building smartphones is useful in the EV market, but I imagine Xiaomi will face the same bottleneck when it works with suppliers like CATL & BYD, they will prioritize Apple and Tesla over Xiaomi because of Apple’s market position and deep pockets.

Overall, I long Xiaomi. Though Xiaomi’s inability to build its own chips and its lack of willingness to vertically integrate the supply chain is worrying. Xiaomi is once again in the right place at the right time, it is bold and it is disrupting. I like that.